Austal reported 34% revenue growth to A$1.1 billion in FY2026 H1 but shares fell 9.05% due to margin concerns

Record order book of A$17.7 billion provides visibility through 2035 but cash flow turned negative

Australasia operations outperformed with 83.5% shipbuilding revenue growth, while U.S. operations faced EBIT decline of 36.8%

Company faces execution challenges translating backlog into profitable growth with target EBIT margins of 7%-9%

📖 Full Retelling

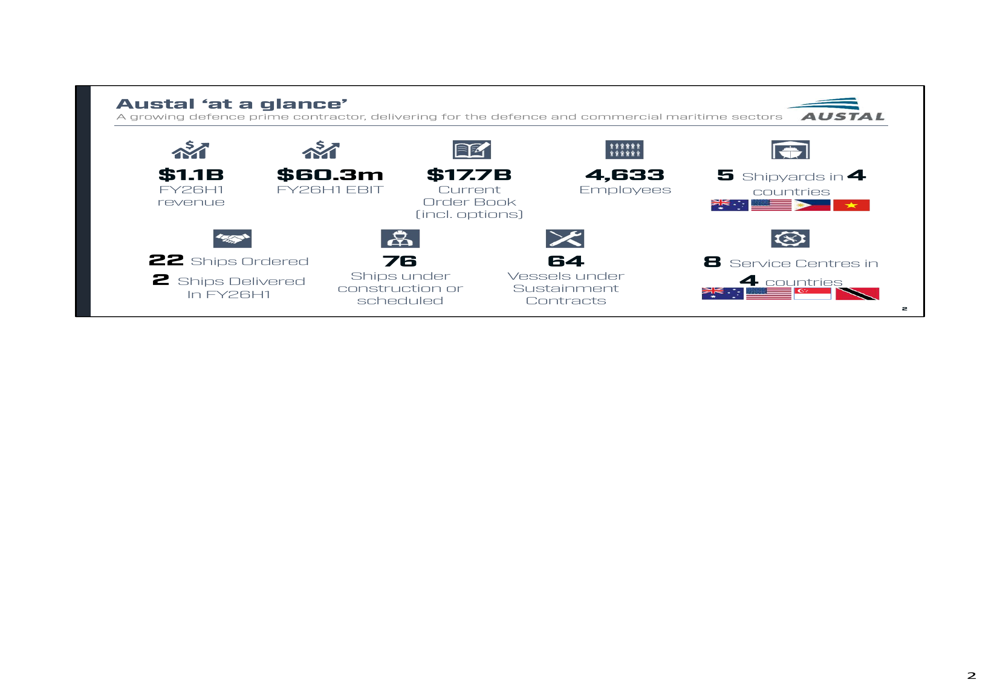

Austal Ltd (ASX:ASB), an Australian shipbuilder, reported a 34% revenue increase for the first half of fiscal 2026 on February 23, 2026, despite facing margin pressures from onerous U.S. contracts and a forecasting error that led to a 9.05% drop in its share price to A$6.30. The company's presentation showcased robust financial metrics with revenue reaching A$1.1 billion, EBIT climbing 41% to A$60.3 million, and net profit after tax rising 21% to A$30.5 million, though these achievements were overshadowed by operational challenges that compressed profitability and strained cash flows. The record A$17.7 billion order book, representing a 35% increase, provides substantial revenue visibility extending through 2035, yet investors remain concerned about the company's ability to translate this backlog into profitable growth given the near-term headwinds.

Geographically, Austal demonstrated varying performance across its operations, with the Australasia region emerging as the standout performer. Shipbuilding revenue in this region surged 83.5% due to increased production on Guardian Class Patrol Boats and Evolved Cape Class Patrol Boats, while U.S. operations faced challenges with shipbuilding EBIT declining 36.8% due to problematic contracts. The segment analysis revealed that the Australasian business now contributes more significantly to overall profitability with a 9.5% EBIT margin compared to 4.9% in the USA, and the Support segment delivered a robust 17.9% EBIT margin versus just 3.1% for Shipbuilding. This divergence highlights the operational disparities between the company's global operations despite the strong overall revenue growth.

Looking ahead, Austal's strategic positioning as a sovereign shipbuilder for Australia and the United States remains strong, supported by extensive contract pipelines in both countries. The U.S. pipeline includes major programs like the Littoral Combat Ship and Expeditionary Fast Transport, while Australian operations have been bolstered by strategic shipbuilding agreements for Landing Craft Medium and Heavy vessels. However, the company faces significant near-term challenges including negative operating cash flow of A$62.9 million and substantial capital expenditure of A$122.5 million for the Module Manufacturing Facility-3 construction. Management aims to achieve target EBIT margins of 7%-9% as new programs stabilize and mature, with the coming quarters critical in demonstrating whether the company can successfully execute on its A$17.7 billion order book while addressing the operational issues that have undermined investor confidence.

Financial tool for tracking orders by buyers and sellers

An order book is the list of orders (manual or electronic) that a trading venue (in particular stock exchanges) uses to record the interest of buyers and sellers in a particular financial instrument. A matching engine uses the book to determine which orders can be fully or partially executed.

Austal's results highlight the critical challenge defense contractors face in balancing strong revenue growth with profitability amid complex government contracts. The sharp stock decline shows investor concern about execution risks despite a record A$17.7 billion order book. This case underscores how operational issues and margin pressures can overshadow positive strategic positioning in the defense sector.

Context & Background

Austal is an Australian shipbuilder with major defense contracts in Australia and the United States

The company reported a 34.4% revenue increase to A$1.1 billion for H1 FY2026

EBIT margin of 5.4% remains below management's 7%-9% target range

Net cash declined 47% and operating cash flow turned negative due to capital expenditures and working capital

The company revised full-year guidance due to a forecasting error on a U.S. contract

What Happens Next

Management will focus on executing the record order book while addressing margin pressures from onerous U.S. contracts. The completion of the Module Manufacturing Facility-3 in May 2026 and San Diego service operations by end of March 2026 are key near-term milestones. Investors will watch for improved cash flow and progress toward the 7%-9% EBIT margin target as new programs mature.

Frequently Asked Questions

Why did Austal's stock price fall despite strong revenue growth?

The stock fell because investors focused on margin pressures from problematic U.S. contracts, negative cash flow, and a guidance revision due to a forecasting error.

What is Austal's main business focus?

Austal primarily focuses on defense shipbuilding, with 96% of its revenue coming from defense contracts for Australia and the United States.

What are Austal's key growth drivers?

Key growth drivers include a record A$17.7 billion order book, strategic shipbuilding agreements with Australia, and expanding U.S. defense programs like the Offshore Patrol Cutter.

}

Original Source

try{ var _=i o; . if(!_||_&&typeof _==="object"&&_.expiry Bitcoin slips after earlier gains amid tariff volatility Can gold rise to new highs above $5,600 in 2026? Bull vs. bear argument on Friday’s Supreme Court tariff ruling 3 key earnings reports for this week to keep the AI trade alive (South Africa Philippines Nigeria) Austal FY2026 H1 slides: 34% revenue surge clouded by margin concerns By Investing.com Company News Published 02/22/2026, 08:51 PM Austal FY2026 H1 slides: 34% revenue surge clouded by margin concerns 0 ASB -10.00% Introduction & Market Context Austal Ltd (ASX:ASB) presented its half-year results for fiscal 2026 on February 23, revealing robust top-line growth tempered by operational challenges that sent shares tumbling 9.05% to A$6.30. The Australian shipbuilder’s presentation showcased a 34% revenue increase and a record A$17.7 billion order book, yet investors focused on margin pressures from onerous U.S. contracts and a guidance revision stemming from a forecasting error. The mixed reception highlights the tension between Austal’s strong strategic positioning as a sovereign shipbuilder for Australia and the United States, and near-term execution challenges that have compressed profitability and strained cash flows. Financial Performance Highlights As shown in the following comprehensive overview of Austal’s key operational metrics, the company demonstrated significant scale across its global operations during the first half of fiscal 2026. Austal reported revenue of A$1.1 billion for the six months ended December 2025, representing a 34.4% increase from the prior corresponding period. EBIT climbed 41% to A$60.3 million, while net profit after tax rose 21% to A$30.5 million. Earnings per share increased 4% to 7.2 cents. The EBIT margin expanded 20 basis points to 5.4%, though this remains well below management’s target range of 7%-9% for mature programs. The company’s order book, including options, surged 35% to A$17.7 billion, providing subst...