Balco Group Q4 2025 slides: Order intake jumps 45%, profitability remains under pressure

#Balco Group #Order Intake #Profitability #Financial Performance #Market Diversification #Structural Reforms #Nordic Markets #Maritime Applications

📌 Key Takeaways

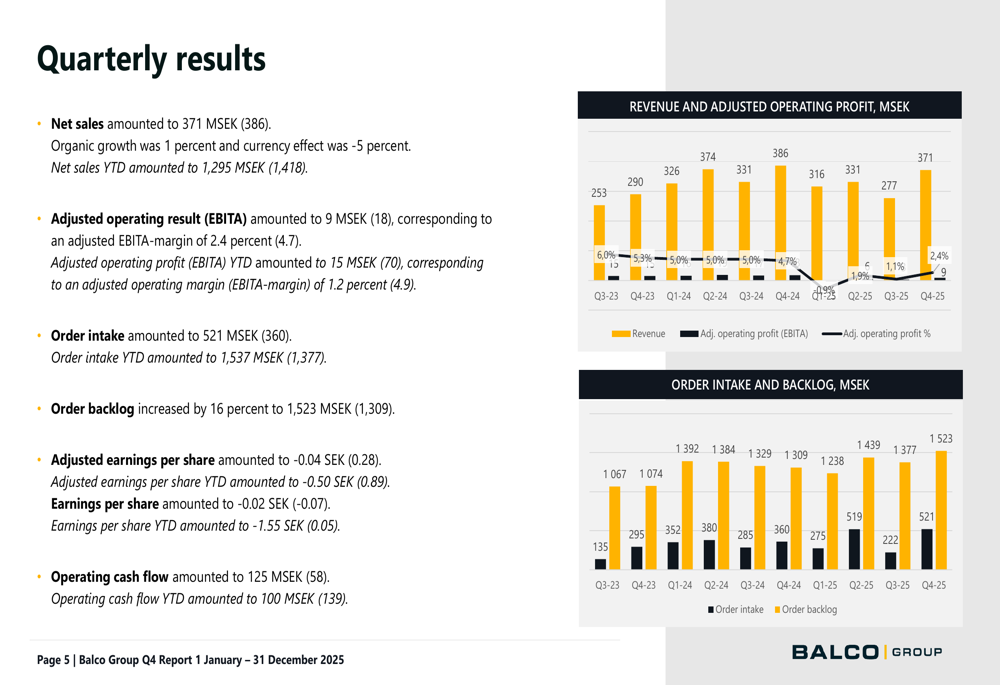

- Balco Group reported a 45% increase in Q4 2025 order intake, reaching 521 MSEK, driven by a record 200 MSEK order for cruise ship components.

- Net sales declined slightly to 371 MSEK in Q4, with organic growth offset by negative currency effects.

- Profitability remained under pressure, with adjusted EBITA falling to 9 MSEK in Q4, representing a margin of 2.4%.

- The company's financial position remains challenging, with interest-bearing net debt in relation to adjusted EBITDA standing at 6.0 times.

- Balco implemented structural cost-saving measures throughout 2025, aiming to improve profitability and diversify its business.

📖 Full Retelling

Balco Group AB, a Nordic balcony solutions specialist, released its fourth quarter and full-year 2025 results on February 6, 2026, showcasing a significant 45% increase in order intake despite ongoing profitability challenges. The company's stock responded positively, rising 6.77% to 17.35 SEK, although it remains well below its 52-week high of 44.05 SEK. Balco has been implementing structural cost-saving measures throughout 2025, aiming to navigate market headwinds and diversify its business beyond residential balconies, including a record order for cruise ship components. The company's order intake surged to 521 MSEK in Q4, up from 360 MSEK in the same period last year, driven by a substantial 200 MSEK order for sliding doors and balconies for cruise ships. However, net sales declined slightly to 371 MSEK, with organic growth offset by negative currency effects. The order backlog increased by 16% to 1,523 MSEK, providing a solid foundation for future revenue. Operating cash flow improved significantly to 125 MSEK, up from 58 MSEK in Q4 2024, strengthening the company's financial position despite elevated debt levels. Profitability remained a challenge, with adjusted EBITA falling to 9 MSEK in Q4, representing a margin of 2.4%, down from 4.7% in the same period last year. For the full year 2025, adjusted EBITA declined to 15 MSEK from 70 MSEK in 2024, with margins dropping to 1.2% from 4.9%. The Renovation segment, which accounts for 78% of total net sales, saw modest revenue growth but experienced a significant decline in profitability. The New Build segment, representing 22% of sales, saw revenue decline but registered impressive order intake growth, with a 75% increase in order backlog. Balco's financial position remains challenging, with interest-bearing net debt in relation to adjusted EBITDA standing at 6.0 times, an improvement from 6.8 times in Q3 but still well above the 2.5 times reported in Q4 2024. The company obtained a waiver and amendment to its existing credit agreement in December to remain in compliance with covenants. Throughout 2025, Balco implemented structural measures aimed at improving profitability, with estimated annual savings of 55 MSEK. The company continues to diversify its geographic presence and expand into maritime applications, which represent a potentially significant growth avenue. On the sustainability front, Balco improved its Sustainalytics risk rating to 16.6, placing it among the top 5% with the lowest risk rating in the 'Building Products' industry. CEO Camilla Ekdahl expressed cautious optimism about order intake for renovation projects in Sweden and Norway in 2026, while noting that Finland will continue to recover at a slower pace. The company expects no clear turnaround in the challenging Danish market and anticipates further growth in Germany and the UK. The maritime business outlook appears positive, with strong order inflow to shipyards and Balco's broader product offering. The Q4 results represent a partial recovery from the company's challenging third quarter, when net sales decreased by 16.3% year-over-year and adjusted EBITDA dropped sharply to 3 MSEK from 17 MSEK. While profitability remains under pressure, the strong order intake and cash flow suggest potential stabilization as the company's cost-saving measures take effect.

🏷️ Themes

Financial Performance, Market Diversification, Profitability Challenges, Structural Reforms

Entity Intersection Graph

No entity connections available yet for this article.