G8 Education 2025 slides: occupancy crisis overshadows quality gains

#G8 Education #Occupancy Crisis #Quality Improvements #Financial Results #Early Childhood Education #Market Challenges #Strategic Priorities #ASX:GEM

📌 Key Takeaways

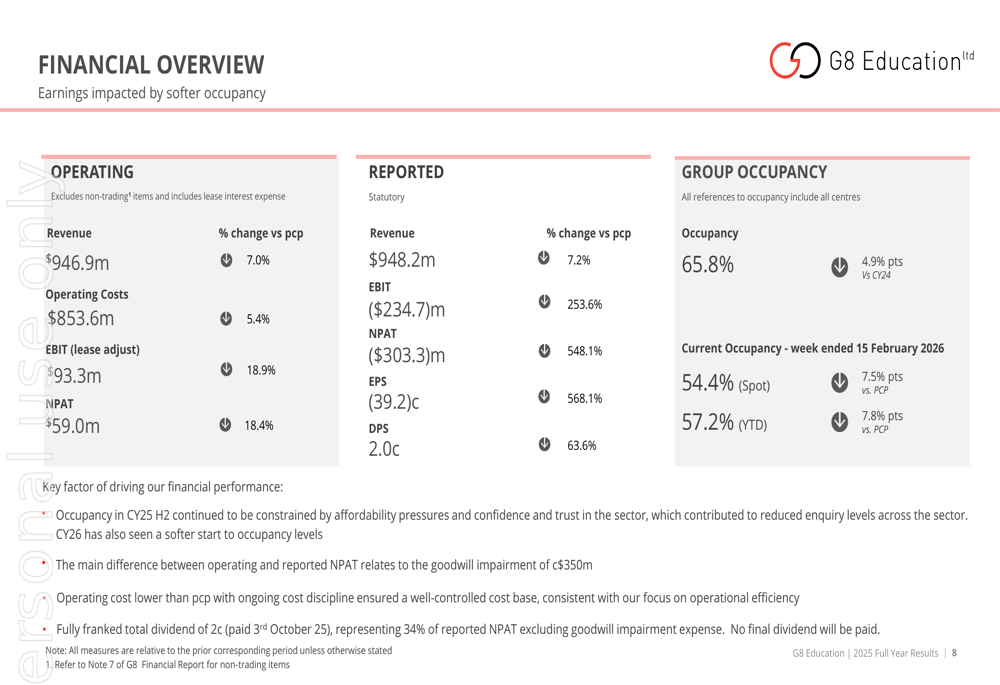

- G8 Education reported a $303.3 million net loss due to $350 million impairment charge despite 7% revenue growth

- Occupancy rates collapsed to 65.8%, down 4.9 percentage points year-over-year with current spot at 54.4%

- Despite occupancy crisis, G8 achieved record Net Promoter Scores and quality ratings above sector average

- Management focusing on safety, team development and quality education to navigate market challenges

📖 Full Retelling

🏷️ Themes

Financial Performance, Educational Quality, Market Challenges, Strategic Management

📚 Related People & Topics

Early childhood education

Teaching of children from birth to age eight

Early childhood education (ECE), also known as nursery education, is a branch of education theory that relates to the teaching of children (formally and informally) from birth up to the age of eight. Traditionally, this is up to the equivalent of third grade. ECE is described as an important period ...

Entity Intersection Graph

No entity connections available yet for this article.

Mentioned Entities

Deep Analysis

Why It Matters

G8 Education's 2025 results highlight a critical challenge in the early childhood education sector where operational excellence is being overshadowed by severe market pressures. The company's 13% stock drop reflects investor concerns that quality improvements cannot overcome collapsing occupancy rates. This situation illustrates broader affordability issues affecting Australian families and the childcare industry's sustainability.

Context & Background

- G8 Education Limited (ASX:GEM) reported full-year 2025 results on February 22, 2026

- Occupancy rates fell sharply to 65.8% in 2025 from 70.7% in 2024, with spot occupancy at 54.4%

- The company reported a statutory net loss of $303.3 million due to a ~$350 million goodwill impairment

- Operational metrics showed strength with record Net Promoter Scores of 53 and 95% of centers meeting quality standards

What Happens Next

G8 will continue facing near-term pressure with current spot occupancy at 54.4% indicating further deterioration. The company's focus on cost management and network optimization through center divestments will aim to preserve cash flow. Recovery timing remains uncertain pending improvement in family affordability and economic conditions.

Frequently Asked Questions

Occupancy declined due to economic headwinds softening enquiry levels, affordability pressures limiting family commitments, and the Child Care Subsidy hourly cap impacting frequency.

G8 achieved record Net Promoter Scores of 53, with 95% of centers meeting or exceeding National Quality Standards, outperforming the sector average by 4 percentage points.

Operating revenue grew 7.0% to $946.9 million, but EBIT margin fell 1.4 percentage points to 9.9%, and a $350 million impairment charge led to a $303.3 million net loss.