Ryder Q4 2025 slides: comparable EPS hits $3.59, outlook remains positive despite market caution

#Ryder System #EPS #Q4 2025 #Freight Market #Logistics #Supply Chain #Earnings Report #Transportation

📌 Key Takeaways

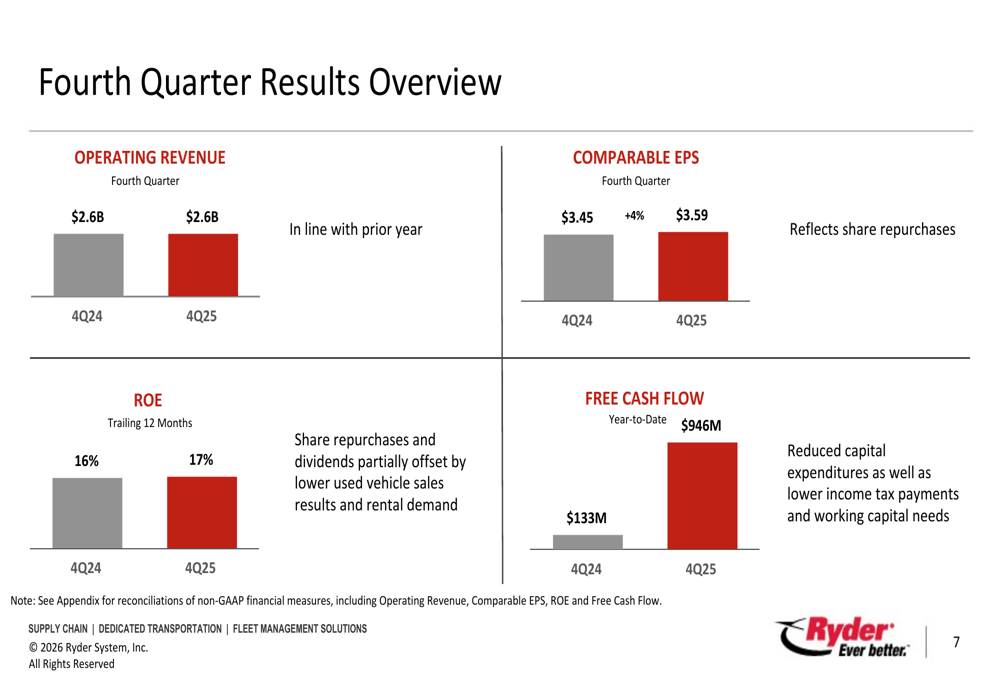

- Ryder reported a fourth-quarter comparable EPS of $3.59, exceeding or meeting market expectations.

- The company's performance was bolstered by long-term contractual services despite a weak freight market.

- Management maintains a positive outlook for 2026, focusing on strategic growth in supply chain and dedicated transport.

- Ryder's focus on capital allocation and shareholder returns remains a priority despite industry-wide caution.

📖 Full Retelling

Ryder System, Inc. reported a comparable earnings per share (EPS) of $3.59 for the fourth quarter of 2025 during an earnings call at its Florida headquarters on February 12, 2026, delivering solid financial results despite a challenging macroeconomic environment and continued stagnation in the freight market. The transportation and logistics giant managed to navigate a period of cautious consumer spending and fluctuating freight volumes, attributes that have historically pressured the company's rental and used vehicle sales divisions. By focusing on contractual lease agreements and dedicated transportation solutions, the company effectively offset the volatility inherent in the broader logistics industry.

The fourth-quarter performance was anchored by the company's strategy to transition toward a more resilient business model, emphasizing its Fleet Management Solutions (FMS) and Supply Chain Solutions (SCS) segments. While the commercial rental market faced typical seasonal headwinds and a surplus of used vehicle inventory across the industry, Ryder's management noted that high-quality maintenance services and long-term leasing contracts provided a stable revenue stream. This diversification has allowed the firm to maintain profitability even as spot rates in the trucking industry remain depressed compared to post-pandemic highs.

Looking ahead, Ryder’s leadership issued a positive outlook for the upcoming fiscal year, signaling confidence in their ability to generate strong free cash flow and deliver value to shareholders through buybacks and dividends. Although the company remains mindful of potential interest rate fluctuations and a slow recovery in the freight cycle, it expects to see continued growth in its e-commerce fulfillment and last-mile delivery sectors. Analysts pointed out that the $3.59 EPS reflects a disciplined approach to cost management and capital allocation, positioning the company as a defensive leader in the transportation sector as it heads into mid-2026.

🏷️ Themes

Logistics, Finance, Corporate Earnings

Entity Intersection Graph

No entity connections available yet for this article.