Waypoint REIT FY25 slides: 3% growth guidance amid portfolio strength

#Waypoint REIT #FY25 results #Distributable earnings #Service stations #Australia property #Viva Energy #Rental income #EV adoption

📌 Key Takeaways

- Waypoint REIT reported 1% FY25 earnings growth with 3% FY26 guidance

- Rental income increased to $165.5 million with 97% tenant retention rate

- Company maintained conservative 32.7% gearing ratio after $50M buyback

- Stock trades at 14.5% discount to NTA with 6.9% distribution yield

- Portfolio shows resilience despite industry headwinds from EV adoption

📖 Full Retelling

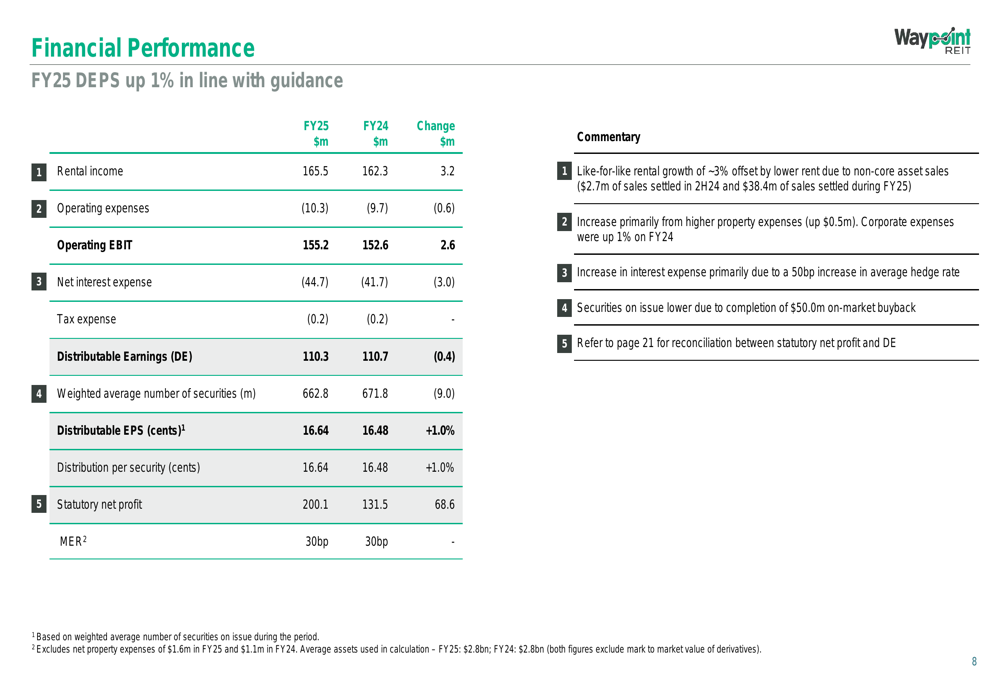

Waypoint REIT Ltd (ASX:WPR) presented its FY25 results on February 25, 2026, delivering distributable earnings per security of 16.64 cents, representing 1.0% growth on FY24, while providing guidance for 3% growth in FY26 amid broader industry headwinds including declining fuel volumes and the gradual adoption of electric vehicles across Australia's vehicle fleet. The company, Australia's largest owner of service station properties with 395 assets valued at $2.86 billion, maintained its portfolio strength despite these challenges, with its stock trading at 2.48 AUD, up 1.21% on the day. The REIT's financial performance showed solid operational results across key metrics for the full year, with rental income increasing by $3.2 million to $165.5 million driven by contractual rent increases and positive leasing outcomes. Operating EBIT rose $2.6 million to $155.2 million, while net interest expense improved by $3.0 million to $44.7 million, reflecting refinancing benefits. Statutory net profit reached $200.1 million, up $68.6 million versus FY24, primarily due to a $102.2 million net gain on property valuation. The company maintained a conservative gearing ratio of 32.7%, positioned at the lower end of its 30-40% target range, following completion of a $50 million on-market buyback program.

🏷️ Themes

Financial Performance, Portfolio Management, Market Positioning, Industry Challenges

📚 Related People & Topics

Viva Energy

Oil company based in Australia

Viva Energy Australia is a listed Australian company that owns the Geelong Oil Refinery and is licensed to retail Shell-branded fuels across Australia under a licence agreement. It also owns and retails fuel through Coles Express, OTR, Reddy Express, Liberty Oil and Westside Petroleum-branded servic...

Entity Intersection Graph

No entity connections available yet for this article.

Mentioned Entities

Original Source

try{ var _=i o; . if(!_||_&&typeof _==="object"&&_.expiry Nasdaq ends more than 1% higher as Nvidia rises pre-earnings, tech extends rebound Gold prices head for fifth day of gains in six; JPMorgan sees more upside Nvidia set to report strong results and guidance, analysts say Nvidia quells AI demand fears with strong revenue guidance, stock up after hours (South Africa Philippines Nigeria) Waypoint REIT FY25 slides: 3% growth guidance amid portfolio strength By Investing.com Company News Published 02/25/2026, 06:50 PM Waypoint REIT FY25 slides: 3% growth guidance amid portfolio strength 0 WPR 1.21% Introduction & Market Context Waypoint REIT Ltd (ASX:WPR) presented its FY25 results on February 25, 2026, delivering distributable earnings per security of 16.64 cents, representing 1.0% growth on FY24, while providing guidance for 3% growth in FY26. The presentation highlighted the company’s resilient portfolio performance despite broader industry headwinds, including declining fuel volumes and the gradual adoption of electric vehicles across Australia’s vehicle fleet. The company’s stock price stood at 2.48 AUD, up 1.21% on the day, trading at a 14.5% discount to its net tangible assets of 2.90 per security. With 395 properties valued at $2.86 billion and a weighted average lease expiry of 6.4 years, Waypoint maintained its position as Australia’s largest owner of service station properties. Financial Performance Highlights As shown in the following detailed financial breakdown, Waypoint delivered solid operational results across key metrics for the full year. Rental income increased by $3.2 million to $165.5 million in FY25, driven by contractual rent increases and positive leasing outcomes. Operating EBIT rose $2.6 million to $155.2 million, while net interest expense improved by $3.0 million to $44.7 million, reflecting the benefits of refinancing activities. The company maintained its management expense ratio at 30 basis points, unchanged from FY23 and FY24. Statu...

Read full article at source