Balco Group Q4 2025 slides: Order intake jumps 45%, profitability remains under pressure

#Balco Group #Order Intake #Profitability #Financial Performance #Market Diversification #Structural Reforms #Nordic Markets #Maritime Applications

📌 Key Takeaways

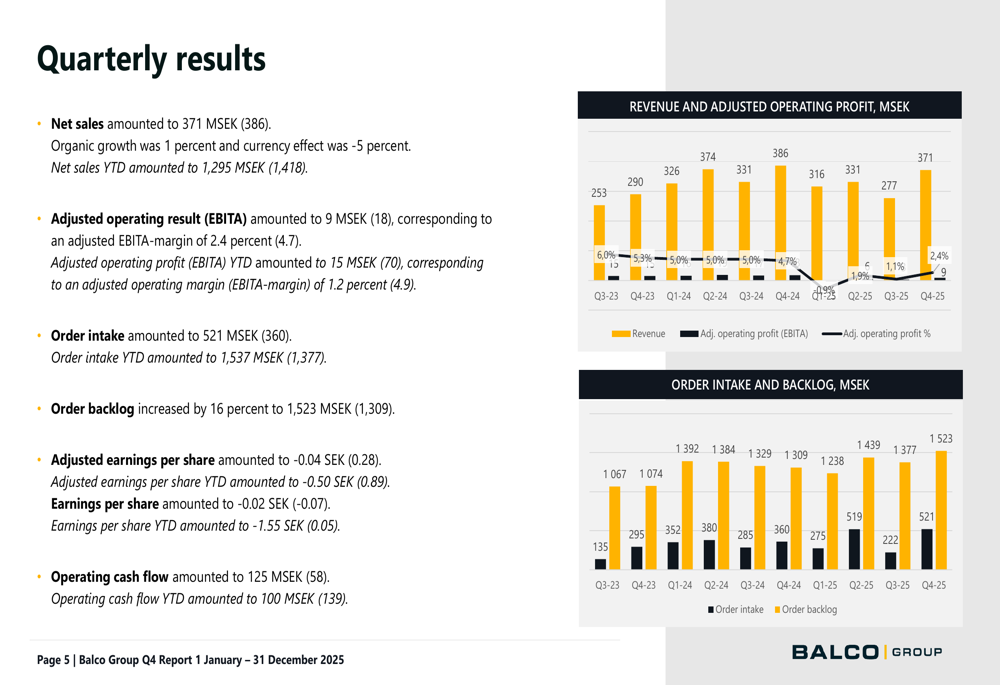

- Balco Group reported a 45% increase in Q4 2025 order intake, reaching 521 MSEK, driven by a record 200 MSEK order for cruise ship components.

- Net sales declined slightly to 371 MSEK in Q4, with organic growth offset by negative currency effects.

- Profitability remained under pressure, with adjusted EBITA falling to 9 MSEK in Q4, representing a margin of 2.4%.

- The company's financial position remains challenging, with interest-bearing net debt in relation to adjusted EBITDA standing at 6.0 times.

- Balco implemented structural cost-saving measures throughout 2025, aiming to improve profitability and diversify its business.

📖 Full Retelling

🐦 Character Reactions (Tweets)

Skeptical InvestorBalco's Q4 report: 45% more orders but profitability still playing hide and seek. Maybe it’s time to send the profits a postcard? #JustHangingOut

Market WatchdogBalco’s got more orders than a busy restaurant on a Friday night, but the profit margins are still thinner than my patience. 🍽️ #BalconyBlues

Debt NavigatorBalco Group's debt-to-EBITDA ratio is like a rollercoaster: thrilling but probably not the safest ride at the fair. 🎢 #DebtStruggles

Sustainability EnthusiastBalco improved its risk rating but let’s be real, it still feels like they’re balcony-ing over a cliff with that profitability! #SustainableButNotProfitable

💬 Character Dialogue

🏷️ Themes

Financial Performance, Market Diversification, Profitability Challenges, Structural Reforms

📚 Related People & Topics

Profit (economics)

Concept in economics

In economics, profit is the difference between revenue that an economic entity has received from its outputs and total costs of its inputs, also known as "surplus value". It is equal to total revenue minus total cost, including both explicit and implicit costs. It is different from accounting profit...

🔗 Entity Intersection Graph

Connections for Profit (economics):

- 🏢 Canaccord Genuity (1 shared articles)

- 🌐 Revenue (1 shared articles)

- 🌐 Manufacturing (1 shared articles)

- 🏢 Earnings report (1 shared articles)

- 🌐 Mytheresa (1 shared articles)

📄 Original Source Content

Balco Group Q4 2025 slides: Order intake jumps 45%, profitability remains under pressure Balco Group AB reported its fourth quarter and full-year 2025 results on February 6, 2026, highlighting strong order intake and cash flow despite continued profitability challenges. The stock responded positively to the presentation, rising 6.77% to 17.35 SEK, though still trading significantly below its 52-week high of 44.05 SEK. The Nordic balcony solutions specialist, which has been implementing structural cost-saving measures throughout 2025, showed signs of recovery in certain markets while continuing to face headwinds in others. The company’s record order for cruise ship components signals potential diversification beyond its core residential balcony business. Balco reported a substantial 45% increase in Q4 order intake to 521 MSEK, compared to 360 MSEK in the same period last year. This included the company’s largest-ever order of approximately 200 MSEK for sliding doors and balconies for cruise ships. For the full year, order intake grew 12% to 1,537 MSEK. Despite the strong order growth, net sales declined slightly to 371 MSEK, with organic growth of 1% offset by a negative currency effect of 5%. The company’s order backlog increased by 16% to 1,523 MSEK, providing visibility for future revenue. Operating cash flow reached 125 MSEK in Q4 compared to 58 MSEK in the same quarter last year, help strengthening the company’s financial position, though debt levels remain elevated. Profitability continued to be a challenge for Balco in Q4, with adjusted EBITA falling to 9 MSEK, representing a margin of 2.4%. For the full year 2025, adjusted EBITA declined to 15 MSEK from 70 MSEK in 2024, with margins dropping to 1.2% from 4.9%. The Renovation segment, which accounts for 78% of total net sales, saw modest revenue growth to 290 MSEK but experienced a significant decline in profitability. Adjusted EBITA for this segment fell to 7 MSEK, with margins dropping to 2.6%. The New...