DocuSign Q4 FY26 slides: billings top $1B, IAM gains momentum

#DocuSign #Q4 FY26 #billings #IAM #electronic signature #digital transaction #revenue #growth

📌 Key Takeaways

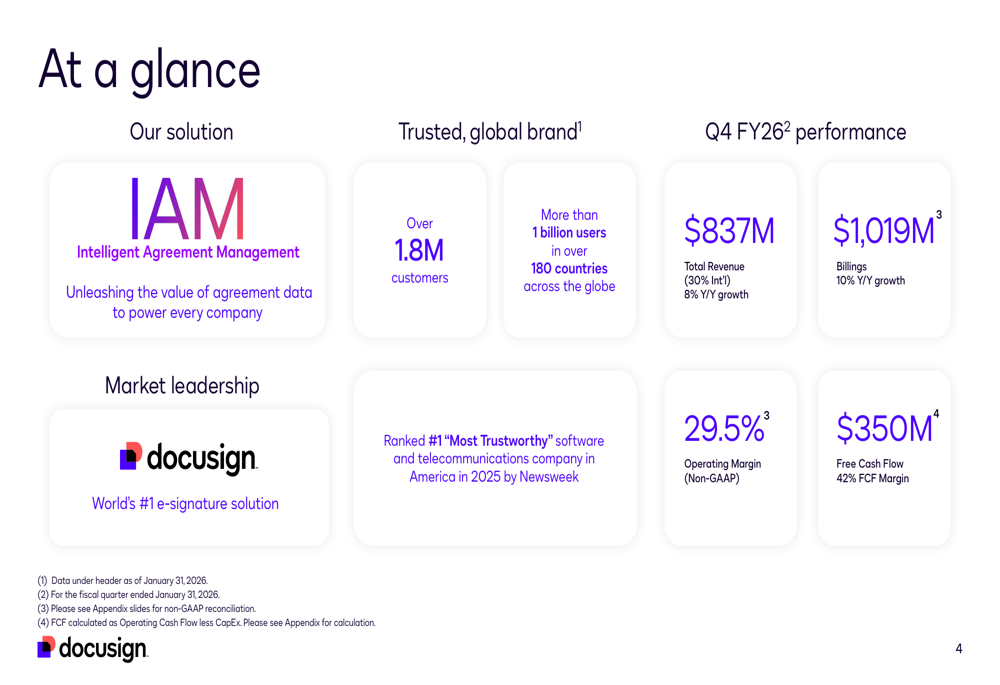

- DocuSign's Q4 FY26 billings exceeded $1 billion, marking a significant financial milestone.

- The company's Identity and Access Management (IAM) segment is showing increased growth and adoption.

- The results reflect strong performance in the electronic signature and agreement management sector.

- DocuSign continues to expand its product offerings and market reach in digital transaction management.

🏷️ Themes

Financial Performance, Technology Growth

📚 Related People & Topics

Docusign

American software company

Docusign, Inc. is an American software company headquartered in San Francisco, California that provides products for organizations to manage electronic agreements with electronic signatures on different devices. As of 2025, Docusign has about 1.7 million clients in 180 countries.

Entity Intersection Graph

No entity connections available yet for this article.

Mentioned Entities

Deep Analysis

Why It Matters

DocuSign surpassing $1 billion in quarterly billings represents a significant milestone for the e-signature and agreement management industry, demonstrating strong enterprise adoption and growth in digital transformation tools. This matters to investors, shareholders, and competitors as it signals DocuSign's continued market leadership and financial health. The momentum in Identity and Access Management (IAM) expansion affects cybersecurity professionals and IT decision-makers who rely on integrated security solutions for digital workflows. The results also impact the broader SaaS sector by setting performance benchmarks and indicating enterprise spending trends on digital agreement platforms.

Context & Background

- DocuSign pioneered the electronic signature market and went public in 2018, becoming synonymous with digital agreement management

- The company has expanded beyond e-signatures into broader 'Agreement Cloud' offerings including contract lifecycle management and analytics

- IAM integration represents DocuSign's strategic move into adjacent security markets to create more comprehensive workflow solutions

- Previous quarters showed steady growth but faced challenges from increased competition from Adobe Sign, Dropbox Sign, and native platform solutions

- The FY26 designation refers to DocuSign's fiscal year ending January 2026, following technology industry fiscal calendar conventions

What Happens Next

Analysts will likely revise upward price targets and earnings estimates following the strong Q4 results, with investor attention shifting to Q1 FY27 guidance expected in the next earnings report. DocuSign will probably accelerate IAM product development and marketing initiatives to capitalize on reported momentum, potentially through acquisitions or partnerships. The company may face increased regulatory scrutiny as it expands into identity management, with potential compliance requirements around data privacy and authentication standards. Competitors like Adobe and newer entrants will likely respond with enhanced security integrations of their own in the coming quarters.

Frequently Asked Questions

Billings exceeding $1 billion indicates strong future revenue recognition and customer commitment, as billings represent contracted revenue that will be recognized over time. This metric suggests healthy sales pipeline and enterprise contract values, which is particularly important for subscription-based SaaS companies like DocuSign.

IAM expansion helps DocuSign move beyond basic e-signatures into more comprehensive security and workflow solutions, creating additional revenue streams and reducing competitive pressure. Integrated identity management enhances document security and compliance, making the platform more valuable for regulated industries like finance and healthcare.

The $1+ billion billing milestone represents accelerated growth from previous quarters, suggesting successful execution of expansion strategies and possibly market share gains. The specific IAM momentum indicates successful cross-selling to existing customers and penetration into new security-conscious market segments.

DocuSign faces ongoing competition from larger tech platforms integrating similar functionality, potential regulatory changes affecting digital signatures, and economic sensitivity if enterprise spending contracts. The expansion into IAM also brings new cybersecurity responsibilities and potential liability exposures that must be managed carefully.

Strong billings and IAM momentum typically drive positive investor sentiment, potentially leading to stock appreciation if guidance remains optimistic. However, the market will also consider valuation metrics and whether growth justifies current price levels, especially if broader tech sector conditions change.