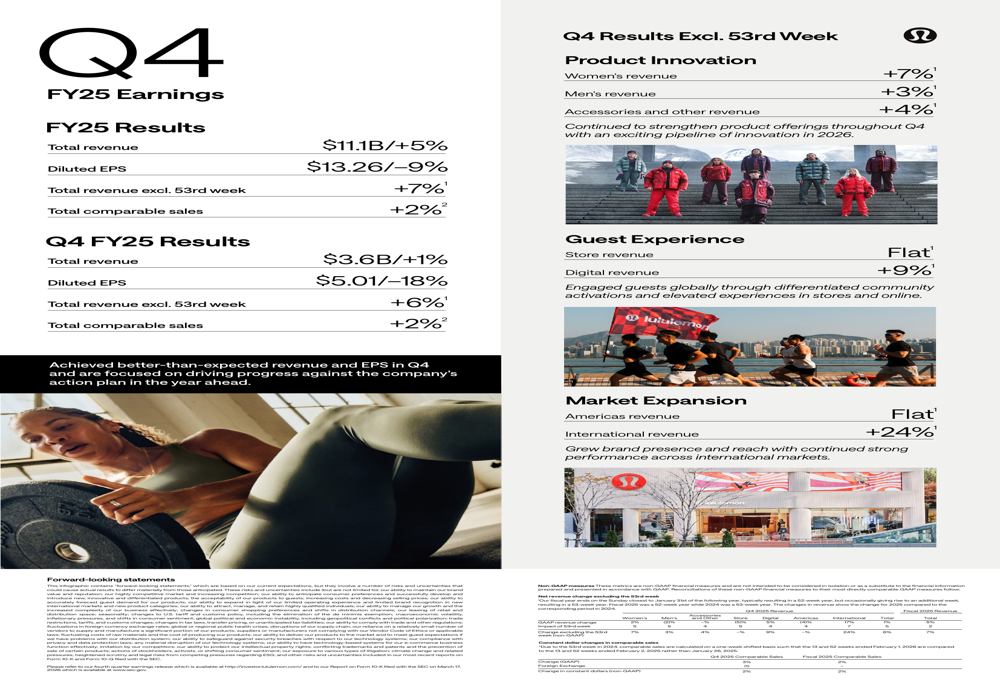

Lululemon Q4 FY25 slides: revenue beats amid profitability pressure

#Lululemon #Q4 FY25 #revenue beat #profitability pressure #earnings slides #financial results #retail sector

📌 Key Takeaways

- Lululemon's Q4 FY25 revenue exceeded analyst expectations

- The company faced pressure on profitability despite revenue growth

- Earnings slides indicate mixed financial performance for the quarter

- Market focus remains on balancing top-line growth with margin management

🏷️ Themes

Earnings Report, Retail Performance

📚 Related People & Topics

Lululemon

Multinational athletic apparel retailer

Lululemon, commonly styled as lululemon ( loo-loo-LEM-ən; all lowercase), is an American-Canadian multinational athletic apparel retailer headquartered in Vancouver, British Columbia, and incorporated in Delaware, United States, as Lululemon Athletica Inc. It was founded in 1998 as a retailer of yo...

Entity Intersection Graph

Connections for Lululemon:

Mentioned Entities

Deep Analysis

Why It Matters

This news matters because Lululemon is a bellwether for the athleisure and premium apparel sectors, indicating consumer spending trends in discretionary categories. The revenue beat suggests continued brand strength and customer loyalty despite economic pressures, while profitability concerns signal potential margin compression that could affect investor returns. This affects shareholders, retail competitors, and supply chain partners who depend on Lululemon's performance, as well as consumers who may see pricing changes.

Context & Background

- Lululemon has grown from a yoga-focused retailer to a global athleisure brand with a market cap exceeding $40 billion

- The company has consistently posted double-digit revenue growth for years, expanding into men's wear, footwear, and international markets

- Recent quarters have shown pressure from increased competition from Nike, Alo Yoga, and emerging direct-to-consumer brands

- The athleisure market surged during the pandemic but faces normalization as consumer habits shift post-COVID

What Happens Next

Analysts will scrutinize the upcoming earnings call for details on margin drivers and guidance for FY26. Investors will watch for cost-control measures or potential price adjustments. Competitors may adjust strategies based on Lululemon's performance, and the stock could see volatility depending on forward-looking statements.

Frequently Asked Questions

It means Lululemon's sales exceeded analyst expectations for Q4 FY25, but its profit margins likely contracted due to factors like higher costs, discounts, or operational expenses.

Profitability can decline despite revenue growth due to rising costs of goods, increased marketing spend, supply chain issues, or competitive pricing pressures that squeeze margins.

The stock may react mixedly—initially up on revenue beat but potentially down if profitability concerns overshadow top-line growth, depending on investor focus on long-term margins.

FY25 refers to Lululemon's fiscal year 2025, which typically runs from February 2024 to January 2025, with Q4 covering the holiday season period.

Key competitors include Nike, Adidas, Athleta, Alo Yoga, and Under Armour, along with emerging digital-native brands in the activewear space.