Worley H1 FY26 slides: revenue rises 5.4% as restructuring weighs

#Worley #H1 FY26 results #revenue growth #restructuring costs #energy transition #EBITA margin #bookings surge #transformation program

📌 Key Takeaways

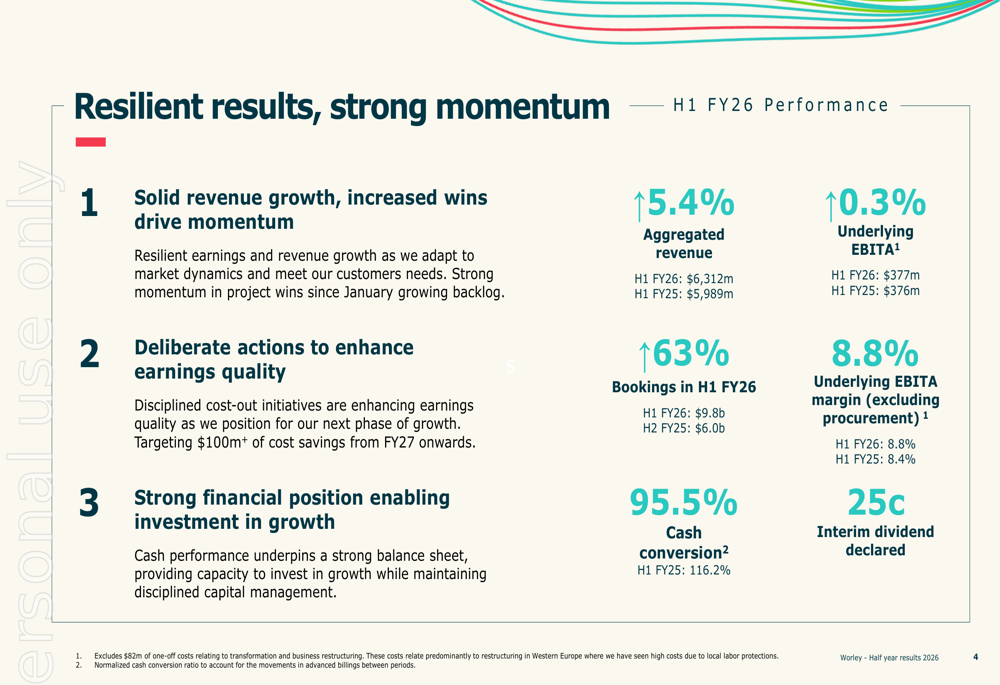

- Worley reported 5.4% revenue growth to $6.3 billion in H1 FY26 but stock fell 7.67% due to restructuring costs

- Underlying EBITA remained flat at $377 million while statutory net profit fell 29.6% to $152 million

- Energy segment grew 8.8% and resources segment grew 12.3%, but chemicals segment declined 9.0%

- Bookings surged 63% to $9.8 billion with sole-sourced wins rising to 48% of total bookings

- Company is undergoing transformation targeting $100 million in annualized savings and positioning for 'Ambition 2.0' growth phase

📖 Full Retelling

Worley Ltd (ASX:WOR) presented its half-year fiscal 2026 results on February 26, revealing a 5.4% year-over-year revenue increase to $6.3 billion, though the engineering services provider's stock declined 7.67% as investors digested $82 million in restructuring costs that weighed on statutory earnings during the company's significant transformation period. The underlying EBITA remained essentially flat at $377 million, rising just 0.3% despite the revenue increase, while the underlying EBITA margin excluding procurement improved to 8.8% from 8.4%, suggesting better quality earnings from core professional services. Statutory net profit after tax and amortization fell 29.6% to $152 million, heavily impacted by the one-time transformation charges, though the company maintained its commitment to shareholders with an interim dividend of 25 cents per share and a $158 million share buyback program.

Worley's diversified business model produced divergent results across its three core sectors, with the energy segment emerging as the strongest performer, revenue climbing 8.8% to $3.18 billion driven by major integrated gas and oil projects. The resources segment also delivered robust growth, up 12.3% to $1.80 billion, supported by strong demand for copper, battery materials, and fertilizer projects. However, the chemicals segment faced significant headwinds, with revenue declining 9.0% to $1.33 billion due to regional imbalances, capacity shifts, and global overcapacity in petrochemicals. A standout highlight was the dramatic 63% increase in bookings to $9.8 billion, with sole-sourced wins rising to 48% of total bookings, reflecting growing customer confidence and competitive positioning.

Central to Worley's H1 FY26 story is an ambitious transformation program designed to enhance long-term competitiveness and margin profile, with the company targeting over $100 million in annualized savings through multiple initiatives including removing organizational complexity, improving efficiency, and embedding artificial intelligence into workflows. The company outlined an ambitious strategic framework built on three pillars: strengthen, expand, and innovate, positioning for what management calls 'Ambition 2.0'—a next phase of growth extending beyond traditional markets. Approximately 69% of revenue is now sustainability-related, positioning Worley favorably for energy transition and decarbonization trends. Despite near-term margin pressure, Worley reaffirmed its full-year FY26 guidance, expecting higher aggregated revenue growth than FY25 and an underlying EBITA margin within a range of 9.0% to 9.5% on a constant currency basis.

🏷️ Themes

Financial Performance, Sector Analysis, Strategic Transformation, Market Outlook

📚 Related People & Topics

Entity Intersection Graph

No entity connections available yet for this article.

Original Source

try{ var _=i o; . if(!_||_&&typeof _==="object"&&_.expiry Nasdaq ends more than 1% higher as Nvidia rises pre-earnings, tech extends rebound Gold prices head for fifth day of gains in six; JPMorgan sees more upside Nvidia set to report strong results and guidance, analysts say Nvidia quells AI demand fears with strong revenue guidance, stock up after hours (South Africa Philippines Nigeria) Worley H1 FY26 slides: revenue rises 5.4% as restructuring weighs By Investing.com Company News Published 02/25/2026, 07:35 PM Worley H1 FY26 slides: revenue rises 5.4% as restructuring weighs 0 WOR -6.98% Introduction & Market Context Worley Ltd (ASX:WOR) presented its half-year fiscal 2026 results on February 26, revealing a company navigating significant transformation while delivering steady top-line growth. The engineering services provider reported aggregated revenue of $6.3 billion, up 5.4% year-over-year, though the stock declined 7.67% to close at $13.04 as investors digested $82 million in restructuring costs that weighed on statutory earnings. The presentation highlighted a company in transition, investing heavily to reset its cost base while capitalizing on strong demand across its energy and resources segments. Despite flat underlying earnings growth of just 0.3%, management emphasized robust bookings momentum and a strategic repositioning designed to unlock future margin expansion. Financial Performance Highlights As shown in the following summary of key financial metrics, Worley delivered resilient results across most operational measures despite challenging market conditions in its chemicals segment. The company’s underlying EBITA of $377 million remained essentially flat year-over-year, rising just 0.3% despite the revenue increase. More notably, the underlying EBITA margin excluding procurement improved to 8.8% from 8.4%, suggesting better quality earnings from core professional services. However, statutory net profit after tax and amortization fell 29.6% to $15...

Read full article at source