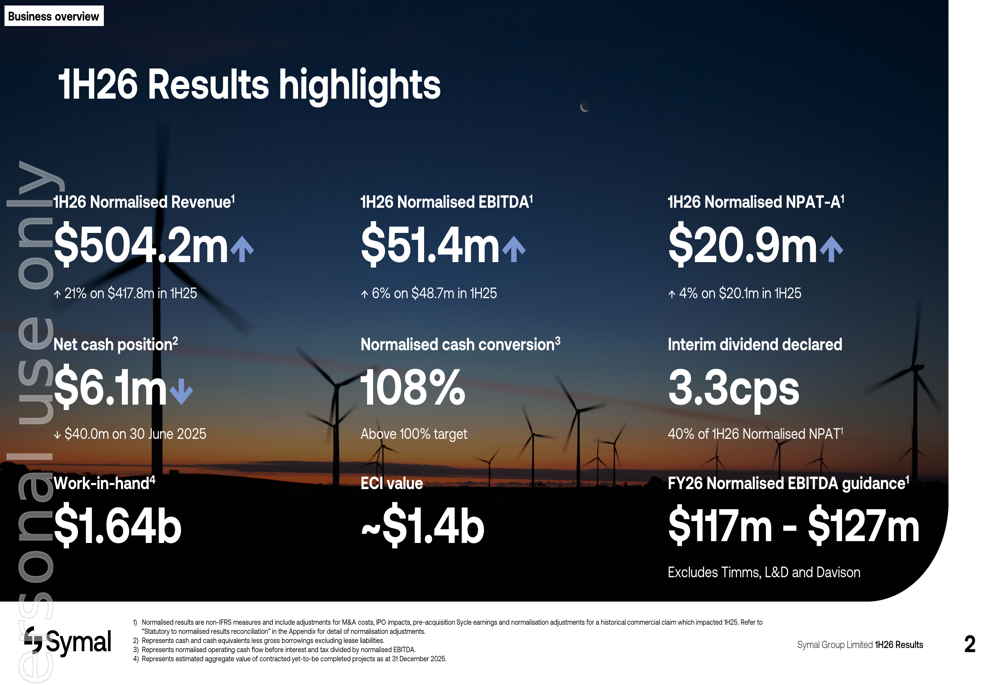

Symal achieved 21% revenue growth to $504.2 million in 1H 2026

EBITDA margins contracted to 10.2% from 11.7% despite rising 6%

Company completed five acquisitions since IPO, reducing net cash position

Management reaffirmed FY26 EBITDA guidance of $117-127 million

Stock declined 25% following results due to margin concerns

📖 Full Retelling

ASX-listed Australian construction and infrastructure contractor Symal Group Ltd presented its first-half fiscal 2026 results on February 22, 2026, revealing robust revenue growth of 21% to $504.2 million amid margin pressure and increased leverage from an aggressive acquisition strategy targeting high-growth sectors. The company's stock declined sharply by approximately 25% to $2.47 following the announcement, reflecting investor concerns about profitability trends despite the impressive top-line performance. The half-year results covered the period ending December 31, 2025, and marked a significant expansion phase for the founder-led company, which has completed five acquisitions since its IPO to build geographic scale and capability depth in data centers, renewable energy, and defense infrastructure. Financial performance showed normalized EBITDA rising 6% to $51.4 million while normalized NPAT increased just 4% to $20.9 million, with EBITDA margin contracting to 10.2% from 11.7% in the prior corresponding period, though still within the company's committed 10-12% target range. The company maintained strong cash conversion at 108%, exceeding its 100% target, while work-in-hand stood at $1.64 billion with an additional $1.4 billion in early contractor involvement projects providing future revenue visibility. Symal declared an interim dividend of 3.3 cents per share, representing 40% of normalized NPAT, though net cash position declined to $6.1 million primarily due to acquisition activity totaling over $50 million for recent transactions including Timms, L&D, and Davison. The company's two operating segments showed divergent performance trends, with the Contracting Services division (83% of revenue) demonstrating 26.5% revenue growth to $419.3 million but with EBITDA margin compression to 6.4%, while the Plant and Equipment segment (17% of revenue) showed more modest 5% revenue growth to $87.3 million but with EBITDA declining 7.1% to $21.3 million as the company invested heavily in fleet expansion. Management reaffirmed FY26 normalized EBITDA guidance of $117-127 million, excluding contributions from recent acquisitions, representing continued growth from the $102.3 million FY25 prospectus base, though the significant stock price decline suggests investors remain concerned about near-term margin pressure, integration execution risk, and the pace of leverage reduction.

Earnings before interest, taxes, depreciation, and amortization, commonly known as EBITDA ( EE-bit-dah, EB-it-dah), is a measure of a company's profitability of the operating business only, thus before any effects of indebtedness, state-mandated payments, and costs required to maintain its asset bas...

Symal's strong revenue growth demonstrates robust demand in infrastructure sectors like data centers and renewable energy, but the sharp stock decline highlights investor concern over profitability and the risks of an aggressive acquisition strategy. The company's performance is a key indicator for the Australian construction sector and its ability to capitalize on major projects like the 2032 Brisbane Olympics.

Context & Background

Symal is an Australian construction and infrastructure contractor listed on the ASX

The company completed five acquisitions since its IPO, expanding into data centers, renewables, and defense

First-half fiscal 2026 revenue reached $504.2 million, up 21% year-over-year

What Happens Next

Symal reaffirmed its full-year EBITDA guidance of $117-127 million, excluding contributions from recent acquisitions. The company will focus on integrating its acquisitions and executing on its pipeline of work-in-hand worth $1.64 billion to restore investor confidence.

Frequently Asked Questions

Why did Symal's stock price fall despite revenue growth?

The stock fell due to investor concerns about margin compression, increased leverage from acquisitions, and slower profit growth compared to revenue growth.

What are Symal's key growth sectors?

Key growth sectors include data centers, renewable energy infrastructure, defense projects, and preparations for the 2032 Brisbane Olympics.

What was Symal's EBITDA margin for the first half?

Symal's EBITDA margin was 10.2%, down from 11.7% in the prior period, but within the company's target range of 10-12%.

Original Source

try{ var _=i o; . if(!_||_&&typeof _==="object"&&_.expiry Bitcoin slips after earlier gains amid tariff volatility Can gold rise to new highs above $5,600 in 2026? Bull vs. bear argument on Friday’s Supreme Court tariff ruling 3 key earnings reports for this week to keep the AI trade alive (South Africa Philippines Nigeria) Symal 1H 2026 slides: revenue surges 21% amid margin pressure By Investing.com Company News Published 02/22/2026, 07:28 PM Symal 1H 2026 slides: revenue surges 21% amid margin pressure 0 SYL -23.17% Introduction & Market Context Australian construction and infrastructure contractor Symal Group Ltd (ASX:SYL) presented its first-half fiscal 2026 results on February 22, revealing robust revenue expansion tempered by margin compression and strategic investment costs. The presentation disclosed normalized revenue of $504.2 million, up 21% year-over-year, though the company’s stock declined sharply by approximately 25% to $2.47 following the announcement, reflecting investor concerns about profitability trends and increased leverage from an aggressive acquisition strategy. The half-year ended December 31, 2025, marked a period of significant expansion for the founder-led company, with five acquisitions completed since its IPO and a strategic push into high-growth sectors including data centers, renewable energy, and defense infrastructure. Financial Performance Highlights As shown in the company’s results summary, Symal delivered strong top-line growth while maintaining cash conversion above its 100% target. The 21% revenue increase to $504.2 million was accompanied by more modest growth in profitability metrics. Normalized EBITDA rose 6% to $51.4 million, while normalized NPAT attributable increased just 4% to $20.9 million. The EBITDA margin contracted to 10.2% from 11.7% in the prior corresponding period, though management emphasized this remains within the company’s committed 10-12% target range. Cash conversion reached 108%, exceeding the company’...